Da Vinci Derivatives-style probability and math-puzzle questions in the style of their OA — with full solutions.

- Free preview

- Full worked solutions

- Easy

- Medium

Da Vinci Derivatives is an Amsterdam-based options market-maker, and its OA is built around probability and math-puzzle questions. The examples below match that style. The later stages — HR rounds, technical interviews, and a superday — go deeper, with the focus depending on the role.

Sample Questions & Solutions

Each question is a real interview problem. Try it yourself first, the full solution is revealed below.

American vs. European Options

EasyShow solution

American Options

An American option can be exercised at any time up until the expiration date. This flexibility allows the holder to capitalize on favorable market movements at any point during the option's life. For example, if the price of the underlying asset moves significantly in favor of the option holder before the expiration date, the holder can exercise the option to capture the profit immediately.

The ability to exercise at any time provides a strategic advantage, particularly in volatile markets or when the underlying asset pays dividends. For instance, an investor holding an American call option on a dividend-paying stock might choose to exercise the option just before the ex-dividend date to receive the dividend payment.

European Options

In contrast, a European option can only be exercised at the expiration date, not before. This restriction means that the holder must wait until the expiration date to exercise the option, regardless of any favorable movements in the price of the underlying asset during the option's life. As a result, European options typically trade at a discount compared to American options, all else being equal, because they offer less flexibility to the option holder.

European options are often used in markets where the underlying asset is less volatile and the need for early exercise is minimal. The pricing of European options is generally simpler due to the fixed exercise date, making them a popular choice for certain financial models and strategies.

The pricing of American and European options also differs due to the exercise flexibility. The Black-Scholes model, for instance, is primarily used for pricing European options and assumes constant volatility and a constant interest rate. American options, however, require more complex models, such as the binomial options pricing model, which can accommodate the possibility of early exercise.

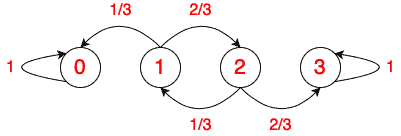

Bankrupt

EasyWhat is the probability that player A wins?

Show solution

The problem starts at state 1. As has been explained in the lessons of this course, we use the following equation:

\begin{equation}

s_1 = \sum_{i=0}^{3}p_{1,i}s_i

\end{equation} \begin{equation}

s_2 = \sum_{i=0}^{3}p_{2,i}s_i

\end{equation} Furthermore, $s_0=0$ and $s_3=1$. Then we have

\begin{equation}

s_1 = \frac{1}{3}*0 + \frac{2}{3} * s_2

\end{equation} \begin{equation}

s_2 = \frac{1}{3}* s_1 + \frac{2}{3} * 1

\end{equation} Solving these equations gives us $s_1=4/7$ and $s_2=6/7$. So, starting with 1 dollar, player A has a 4/7 chance of winning.

Proof

If we substitute Equation 4 in Equation 3, we have

\begin{equation}

s_1 = \frac{1}{3}*0 + \frac{2}{3} * (\frac{1}{3}* s_1 + \frac{2}{3} * 1)

\end{equation} \begin{equation}

s_1 = \frac{2}{9} * s_1 + \frac{4}{9}

\end{equation} \begin{equation}

\frac{7}{9} * s_1 = \frac{4}{9}

\end{equation} \begin{equation}

s_1 = \frac{4}{9} / \frac{7}{9} = \frac{4}{7}

\end{equation}

All Faces

EasyShow solution

n \Sigma_{k=1}^n \frac{1}{k}

\end{equation} which, for large n is approximately n log n.

The time until the first result appears is 1. After that, the random time until a second (different) result appears is geometrically distributed with parameter of success 5/6, hence with mean 6/5 (recall that the mean of a geometrically distributed random variable is the inverse of its parameter). After that, the random time until a third (different) result appears is geometrically distributed with parameter of success 4/6, hence with mean 6/4. And so on, until the random time of appearance of the last and sixth result, which is geometrically distributed with parameter of success 1/6, hence with mean 6/1. This shows that the mean total time to get all six results is \begin{equation}

6 \Sigma_{k=1}^6 \frac{1}{k} = \frac{147}{10} = 14.7

\end{equation}

Fox vs. Duck

MediumCan the duck always reach the shore without being caught by the fox?

Show solution

Once the duck is at an angle of $\pi$ from the fox, it starts swimming towards the shore.

- The duck has to cover a distance of $\frac{3r}{4}$

- The fox has to cover a distance of $\frac{2\pi \cdot r}{2}$

Since the fox moves four times faster, the distance of the fox has to be larger than four times the distance of the duck.

As we can see, \begin{equation}\frac{3r}{4} * 4 < r* \pi \end{equation} \begin{equation} 3r < 3.14r \end{equation} \begin{equation} 3 < 3.14 \end{equation} Therefore, the duck will survive!

Ready for the full question bank?

You just worked through 4 of our free sample questions. Full access unlocks 500+ interview questions, timed mock OAs, progress tracking, and detailed analytics across every trading firm listed above.